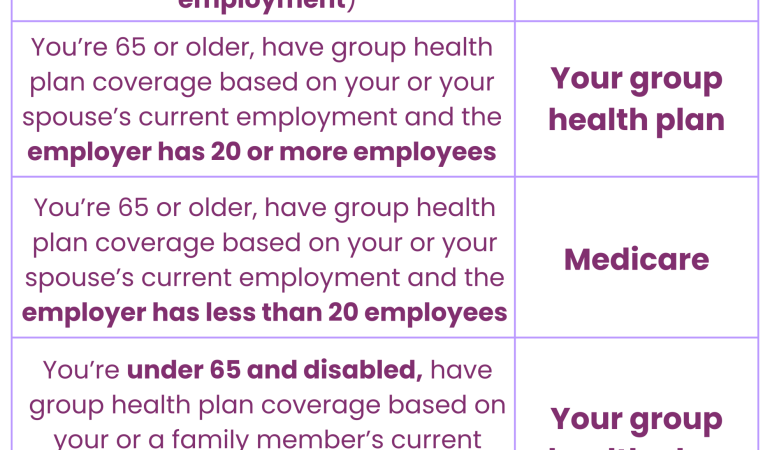

Below is a simplified, easy-to-read breakdown of the rules based on the official Medicare guidance.

Our job is not to sell insurance; it’s to help our clients make an educated decision about their health insurance options.

Below is a simplified, easy-to-read breakdown of the rules based on the official Medicare guidance.