Inpatient hospital care

If a doctor formally admits you to a hospital, Part A will cover you for up to 90 days in your benefit period. This period begins the day you are admitted and ends when you have been out of the hospital for 60 days in a row. Once you meet your deductible, Part A will pay for days 1–60 that you are in the hospital. For days 61–90, you will pay a coinsurance for each day. If you need to stay in the hospital for longer than 90 days, you can use up to 60 lifetime reserve days. These are extra days of Medicare coverage for long hospital stays. However, lifetime reserve days are nonrenewable, and require a daily coinsurance payment.

Skilled Nursing Facility care

Part A will help cover many services in a Skilled Nursing Facility (SNF). This includes room and board, as well as administering medicine or changing sterile dressings. Medicare will cover you for up to 100 days in each benefit period. To qualify for this coverage, you must spend at least 3 days as an inpatient in a hospital within 30 days of being admitted to an SNF.

Hospice care

Hospice care can provide comfort when a patient is terminally ill. Fortunately, there are relatively fewer restrictions on Medicare eligibility for hospice care coverage. As long as your provider certifies the care, Medicare will cover the cost.

Home healthcare

If you need skilled care and are homebound, you could qualify for Medicare coverage for home healthcare. Skilled care generally refers to services that require a license or medical supervision to carry out. Medicare Part A can cover up to 100 days of home healthcare if you spent 3 days or more as a hospital inpatient within 14 days of getting home healthcare.

Premium-free Medicare Part A

Generally, if you’re 65 or older, and you or your spouse worked and paid Medicare taxes for at least 10 years, you’ll pay no premium for Medicare Part A. If you don’t qualify for premium-free Part A, you can still get Original Medicare Part A, but you will have a monthly premium. Your premium will be no more than $565 each month in 2026. This amount depends on how long you or your spouse worked and paid Medicare taxes.

Medicare Part A benefit periods, deductibles and copays

There are other costs for Medicare outside of premiums. Your deductible is the amount you must pay for healthcare before Medicare begins coverage. For Part A inpatient hospital coverage in 2026, this deductible amount is $1,736 for each benefit period.

The Medicare Part A benefit period for a stay in the hospital or an SNF begins the day you are admitted and ends when you have been out of the hospital or SNF for 60 days in a row. You will pay a new deductible with each new benefit period.

Medicare Part A copays change based on the benefit period. Coinsurance payments for Part A during a hospital stay are:

Coinsurance payments for Part A during a skilled nursing facility stay are:

Medicare Part B

Medicare Part B Coverage and Costs:

While Medicare Part A, with its coverage for hospital visits and skilled nursing care, can help you manage the “major stuff,” that’s only part of the picture. Medicare Part B helps you get the care you need for a lot of the day to day “stuff” that requires a doctor’s care. And you can receive care from any doctor who accepts Medicare patients.

Original Medicare Part B helps cover:

Medicare Part B also helps cover a number of preventive services (if you qualify by age, gender or risk factor). These may include:

Medicare Part B premiums

Generally, most 2026 Medicare members must pay a monthly Part B premium of $202.90 (standard premium).

Your Part B premium could be higher depending on your income. If your modified adjusted gross income from 2 years ago is above a certain amount, you’ll pay the standard premium plus what’s called an “Income Related Monthly Adjustment Amount” (IRMAA ). To see if this applies to you, look at your past income tax return to find your modified adjusted gross income there. Compare that figure to the IRMAA chart below.

For most people, paying the premium is simple. Your Part B premium will be automatically deducted from your benefit payment if you get benefits from 1 of these:

Social Security

Railroad Retirement Board

Office of Personnel Management

Medicare Part B deductibles

Like most insurance plans, Medicare Part B does have a standard deductible. In 2026, that deductible is $283. After you meet your deductible for the year, you’ll typically pay 20% of the Medicare-approved amount for most Part B covered services.

Medicare Part B coinsurance

After the deductible, you’ll pay a coinsurance of 20% that will apply to.

Most doctor services (including most doctor services while you’re a hospital inpatient), Outpatient Surgery & Services, Durable Medical Equipment (DME), Ambulance, ER visits and more. These “day to day stuff” mentioned above can add up quickly with no maximum out of pocket or “cap.”

Am I eligible for Medicare Part B?

Most people become eligible for Medicare when they turn 65. Some people may qualify before age 65 due to illness or disability. If you’re ready to explore your Medicare options, you can visit Medicare.gov to verify your eligibility. It’s quick and easy.

When can I enroll in Medicare Part B?

Waiting for your 65th birthday to sign up? Good news! You have time to shop.

Your Initial Enrollment Period begins 3 months before the month of your 65th birthday, includes your birthday month, and continues through the 3 months after the month of your 65th birthday. That gives you 7 months to learn about Medicare and compare plans so you can make the right choice for you.

Worried about Original Medicare Costs?

Medicare helps cover many healthcare expenses, but Original Medicare (Part A and Part B) does not include a maximum out-of-pocket limit. This means costs such as deductibles, copays, and the standard 20% Part B coinsurance can add up quickly – especially with frequent doctor visits, outpatient services, or unexpected medical needs.

For individuals with limited income, Medicare Savings Programs (Medicaid) may help pay Part A or Part B premiums. These state-sponsored programs are based on income and assets and do not change your Medicare benefits or coverage.

If you don’t qualify for assistance, many beneficiaries look at additional coverage options to help manage financial risk. Some choose a Medicare Supplement (Medigap) plan, which helps cover the gaps in Original Medicare, including deductibles and coinsurance. Others consider Medicare Advantage plans, which bundle coverage and include an annual out-of-pocket maximum.

If you’re comparing these coverage options, our Medigap vs Medicare Advantage page explains the key differences in costs, coverage structure, and provider flexibility.

Ultimately, the right Medicare setup depends on your income, healthcare usage, doctor preferences, and comfort with potential out-of-pocket costs.

Medicare Part D

Medicare Part D Coverage and Costs:

There’s two ways to get Part D, either purchase a Stand-Alone Prescription Drug Plan or enroll in a Medicare Advantage Plan that includes Prescription Drug Coverage (aka Part D). Each Medicare Part D plan uses a list of approved drugs to decide what’s covered and what isn’t. This list is called a drug formulary . The formulary may differ from plan to plan. Many plans arrange their list of covered drugs in different levels, called “tiers”. Generally, drugs in a lower tier will cost less than drugs in a higher tier.

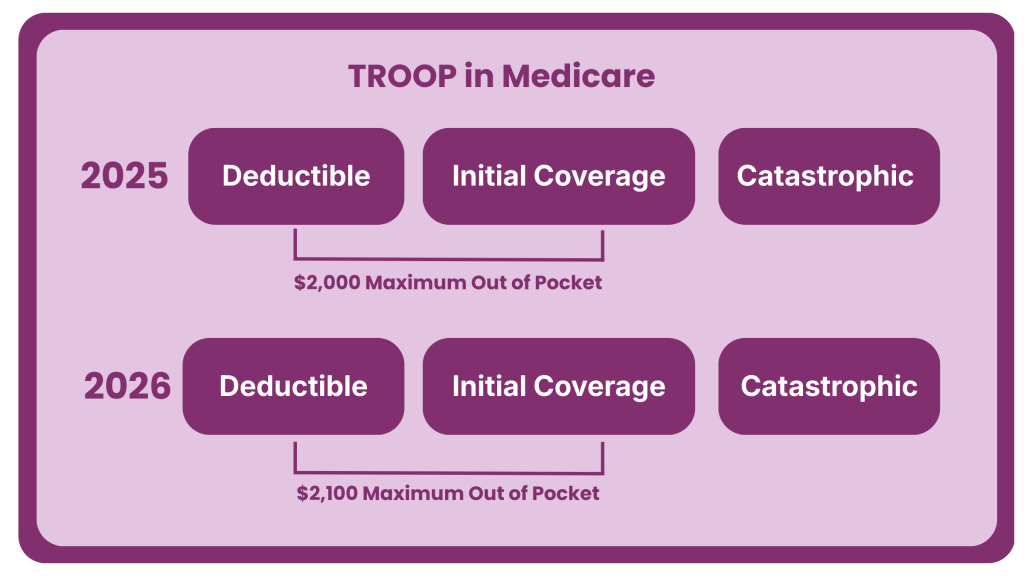

Medicare Part D TrOOP in 2026

TrOOP stands for True Out-of-Pocket costs.

It refers to the amount you personally pay for covered prescription drugs under a Medicare Part D plan during the year.

Once your TrOOP spending reaches a certain limit, you move into the catastrophic coverage phase ($2,100 in 2026), where your drug costs drop significantly.

What counts toward TrOOP

-Your copays and coinsurance for covered drugs

-Your deductible ($0-$615 depending on the plan)

-Manufacturer discounts on brand-name drugs (in the coverage gap)

What does NOT count toward TrOOP

Why TrOOP matters

-It determines when your drug costs decrease

-It affects which Part D plan may be best, especially for high-cost medications

-It’s one of the most commonly misunderstood parts of Medicare

2026 Medicare IRMAA Income Brackets for Part B and Part D

The chart below shows the current Medicare IRMAA income brackets and the additional surcharges that higher-income beneficiaries may pay for Medicare Part B and Part D premiums.

The Medicare IRMAA income brackets shown above determine when higher-income beneficiaries pay additional surcharges for Part B and Part D.

What Is Medicare IRMAA?

Medicare IRMAA (Income-Related Monthly Adjustment Amount) is an additional surcharge that higher-income beneficiaries may pay on top of their standard Medicare Part B and Medicare Part D premiums. The Social Security Administration determines whether IRMAA applies using your modified adjusted gross income (MAGI) from two years prior, based on information from your federal tax return. Many people are aware that IRMAA can increase the monthly premium for Medicare Part B, but fewer realize that it can also add a separate surcharge to Part D prescription drug coverage, even if the drug plan itself has a very low premium. A common mistake is declining Part D coverage simply because IRMAA increases the cost; however, going without creditable prescription drug coverage can later trigger a permanent Medicare Part D Late Enrollment Penalty (LEP) if you enroll in a drug plan in the future. Understanding how Medicare IRMAA works can help you avoid surprises and make better decisions about your long-term Medicare coverage. Because IRMAA thresholds are based on income levels and tax filings from two years prior; changes in income, retirement, or life events may affect whether these Medicare surcharges apply.

Frequently Asked Questions on Medicare Coverage and Costs