Understanding Medicare Supplemental Insurance (Medigap)

Navigating your healthcare options can sometimes feel overwhelming, but understanding how Medicare Supplemental Insurance—commonly known as Medigap—functions can help bridge the gaps in your Medicare coverage. Many individuals turn to Medigap to complement their Original Medicare and gain peace of mind when it comes to out-of-pocket costs. This guide will take you step-by-step through what Medigap is, how it works, and who might benefit from it.

What Is Medigap?

Medigap is private health insurance specifically designed to fill the coverage gaps in Original Medicare (Parts A and B). While Original Medicare covers many costs, like hospital stays and outpatient care, it doesn’t pay for everything. This is where Medigap comes in—it helps cover certain out-of-pocket expenses, such as:

- Deductibles

- Copayments

- Coinsurance

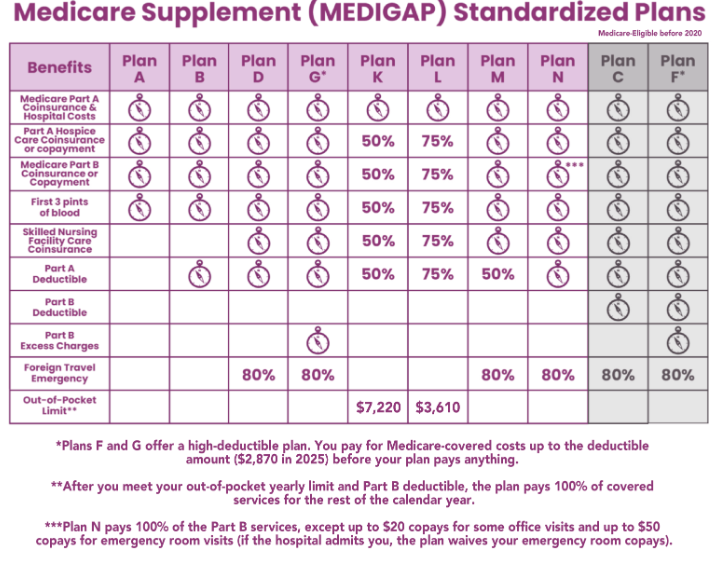

Medigap policies are standardized and labeled as Plans A, B, C, D, F, G, K, L, M, and N. Each plan offers a different level of coverage, making it easier to compare and figure out which one suits you best.

It’s important to note that Medigap only works with Original Medicare. If you’re enrolled in a Medicare Advantage plan, you’re not eligible to use Medigap.

How Does Medigap Work?

Here’s a simple breakdown of how Medigap complements Original Medicare:

- Original Medicare First

When you receive a covered medical service, Original Medicare will pay its share of the approved amount. - Medigap Fills the Gaps

After Medicare pays its portion, your Medigap policy will step in to pay for remaining costs, such as deductibles or copayments.

For example, if you visit the doctor and Medicare covers 80% of the costs, Medigap can help you cover the remaining 20% that you would otherwise have to pay out of pocket.

Some Medigap plans even include additional benefits, like foreign travel emergency coverage, which isn’t included with Original Medicare.

Important Reminder: Medigap policies don’t cover everything. For example:

- They don’t pay for prescription drugs. You’ll need a separate Part D plan for this.

- They don’t cover services such as dental, vision, or hearing care.

Always review what’s included in each Medigap plan before making your choice.

Who Might Benefit from Medigap?

Medigap isn’t for everyone, but it can be a great option depending on your healthcare needs and preferences. Here’s who typically benefits the most:

- Frequent Healthcare Users

If you have chronic conditions or need regular care, Medigap could help reduce your out-of-pocket costs. - Frequent Travelers in the U.S. and abroad

Medigap offers nationwide coverage, unlike some Medicare Advantage plans that only cover in-network providers. Certain plans also provide emergency coverage when traveling outside of the U.S. - Individuals Concerned About High Out-of-Pocket Costs

Medigap policies are designed to protect you against large, unexpected healthcare bills by covering deductibles, copayments, and coinsurance. - Those Who Prefer Simple Coverage

With Medigap, you don’t have to worry about network restrictions. You can visit any doctor or hospital that accepts Medicare.

Medigap Costs and Considerations

Like all insurance, Medigap comes with costs you’ll want to consider. Here’s a brief overview:

- Monthly Premiums

Medigap policies have an additional monthly premium that you’ll pay on top of your Medicare Part B premium. Premiums vary based on the plan type, your insurance provider, and even your age or location. - Out-of-Pocket Costs

While Medigap helps reduce many out-of-pocket costs, it doesn’t pay for everything. Be sure to compare plan details to see what’s covered. - Plan Standardization

Medigap plans with the same letter (e.g., Plan G from one provider vs. Plan G from another) offer the exact same benefits, but premiums may differ based on the company selling the policy. - Timing of Enrollment

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period, which begins the month you’re 65 or older and enrolled in Medicare Part B. During this time, you’ll get the best rates and won’t be denied coverage due to pre-existing conditions.

Key Tip: If you miss this enrollment period, you may face higher costs or difficulty obtaining a policy.

How to Choose the Right Medigap Plan

Selecting the right Medigap plan for your needs involves a few essential steps:

- Assess Your Healthcare Needs

Look at how often you visit the doctor, your medical history, and whether you travel often. - Compare Plans

Review the standardized Medigap plans to find one that fits your budget and coverage needs. - Consider Costs

Balance premium affordability with the out-of-pocket savings you’ll gain. - Research Insurance Providers

Since premiums can vary, compare pricing among different companies offering Medigap plans in your area.

If you’re unsure where to start, consider speaking with a Medicare advisor who can explain your options and help you identify the best solution for your situation.

Final Thoughts

Medigap can be an invaluable tool for those who want added peace of mind and financial protection alongside their Original Medicare coverage. However, every person’s healthcare needs and budget are unique, so take the time to compare options carefully.

Remember, the right plan is out there—it’s just a matter of assessing your priorities and finding a policy that matches your goals.

If you have more questions about Medigap or would like personalized assistance, don’t hesitate to reach out to a Medicare advisor. It’s never too early to start planning for a healthier, stress-free future.

Leave A Comment